During the second quarter of 1988, Buzz Company sold a piece of equipment at a $12,000 gain. What portion of the gain should Buzz report in its income statement for the second quarter of 1988?

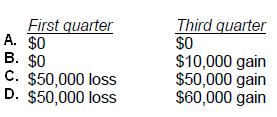

Wilson Corp. experienced a $50,000 decline in the market value of its inventory in the first quarter of its fiscal year. Wilson had expected this decline to reverse in the third quarter, and in fact, the third quarter recovery exceeded the previous decline by $10,000. Wilson's inventory did not experience any other declines in market value during the fiscal year. What amounts of loss and/or gain should Wilson report in its interim financial statements for the first and third quarters?

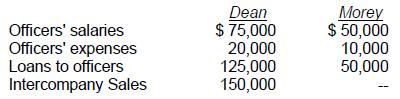

Dean Co. acquired 100% of Morey Corp. prior to 1989. During 1989, the individual companies included in their financial statements the following:

What amount should be reported as related party disclosures in the notes to Dean's 1989 consolidated financial statements?

Reclassification adjustments must be shown in the financial statement that discloses comprehensive income:

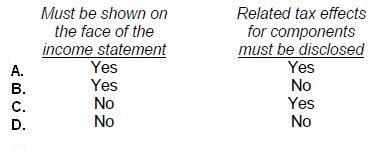

Which of the following is true regarding the presentation of "comprehensive income."